Welcome to our guide on understanding unpaid accrued interest on student loans. One of the common challenges for students and graduates is dealing with accruing interest on their loans. It can be confusing and stressful to see the amount owed increase over time, even if you are making regular payments. In this article, we will break down what accrued interest is, how it affects your loan balance, and ways to manage it effectively. Let’s navigate through this financial maze together!

Understanding Unpaid Accrued Interest on Student Loans

When it comes to student loans, understanding the concept of unpaid accrued interest is essential. Student loans come with interest rates, which are essentially fees charged by the lender for borrowing the money. Accrued interest refers to the interest that builds up over time on the original loan amount. Unpaid accrued interest occurs when the borrower does not make payments to cover the interest as it accrues. This unpaid interest can then be added to the principal balance of the loan, causing the borrower to owe more money in the long run.

Unpaid accrued interest on student loans can have serious consequences for borrowers. As interest continues to accrue, the total amount owed on the loan can grow significantly. This means that borrowers may end up paying much more than the original amount borrowed. Additionally, unpaid accrued interest can also impact the borrower’s credit score, making it harder to secure loans in the future.

There are several reasons why unpaid accrued interest may occur on student loans. One common reason is when borrowers enter into a deferment or forbearance period and do not make any payments on the loan. During these periods, interest continues to accrue, and if left unpaid, can be added to the principal balance of the loan once the deferment or forbearance period ends. Another reason for unpaid accrued interest is when borrowers make only minimum payments on their loans, which may not be enough to cover the accruing interest.

It is important for borrowers to be aware of the implications of unpaid accrued interest on their student loans and to take proactive steps to address the issue. One way to prevent unpaid accrued interest from accumulating is to make payments on the loan regularly, even if they are only able to make the minimum payment. By making consistent payments, borrowers can prevent interest from building up and avoid having it added to the principal balance of the loan.

If borrowers are struggling to make payments on their student loans, it is important to contact their loan servicer as soon as possible. Many loan servicers offer options such as income-driven repayment plans or loan consolidation, which can help borrowers better manage their loans and prevent unpaid accrued interest from becoming a problem.

In conclusion, unpaid accrued interest on student loans is a serious issue that borrowers need to be aware of. By understanding how unpaid accrued interest occurs and taking proactive steps to address it, borrowers can prevent this issue from becoming a major financial burden. It is important for borrowers to stay informed about their loan terms and to communicate with their loan servicer if they are struggling to make payments. By staying proactive and informed, borrowers can better manage their student loans and avoid the negative consequences of unpaid accrued interest.

Impact of Unpaid Accrued Interest on Loan Repayment

Unpaid accrued interest on student loans can have a significant impact on loan repayment for borrowers. When interest accrues on a student loan, it means that the borrower owes more money overall, as interest is calculated based on the remaining principal balance. If this accrued interest remains unpaid, it can lead to several negative consequences for the borrower.

One major impact of unpaid accrued interest is that it can increase the total amount owed on the loan. This means that the borrower will ultimately end up paying more money than they initially borrowed, as the interest continues to compound over time. As a result, the borrower may find it difficult to fully repay the loan, leading to longer repayment terms and higher overall costs.

In addition, unpaid accrued interest can also lead to a higher monthly payment for the borrower. When interest accrues on a loan, the total amount owed increases, which means that the borrower will need to pay more each month to cover the accrued interest as well as the remaining principal balance. This can put a strain on the borrower’s finances, especially if they are already struggling to make ends meet.

Furthermore, unpaid accrued interest can negatively impact the borrower’s credit score. If the borrower is unable to keep up with their monthly payments due to the increased costs of accrued interest, they may default on the loan. This can have a lasting impact on their credit history, making it difficult for them to secure future loans or credit cards. In some cases, defaulting on a loan can even lead to legal action being taken against the borrower.

Overall, unpaid accrued interest on student loans can have a ripple effect on the borrower’s financial situation. It can lead to higher overall costs, increased monthly payments, and potential damage to the borrower’s credit score. To avoid these negative consequences, it is important for borrowers to stay on top of their loan payments and address any accrued interest as soon as possible.

Strategies for Managing Unpaid Accrued Interest on Student Loans

Unpaid accrued interest on student loans can be a burden for many borrowers, but there are several strategies that can help manage this situation effectively. Here are some tips to help you navigate through this challenging financial hurdle:

1. Make Interest-Only Payments: One of the most common strategies for managing unpaid accrued interest on student loans is to make interest-only payments. By paying only the interest that has accrued on your loan, you can prevent it from capitalizing and increasing the overall balance. This can help you avoid a larger debt burden in the long run.

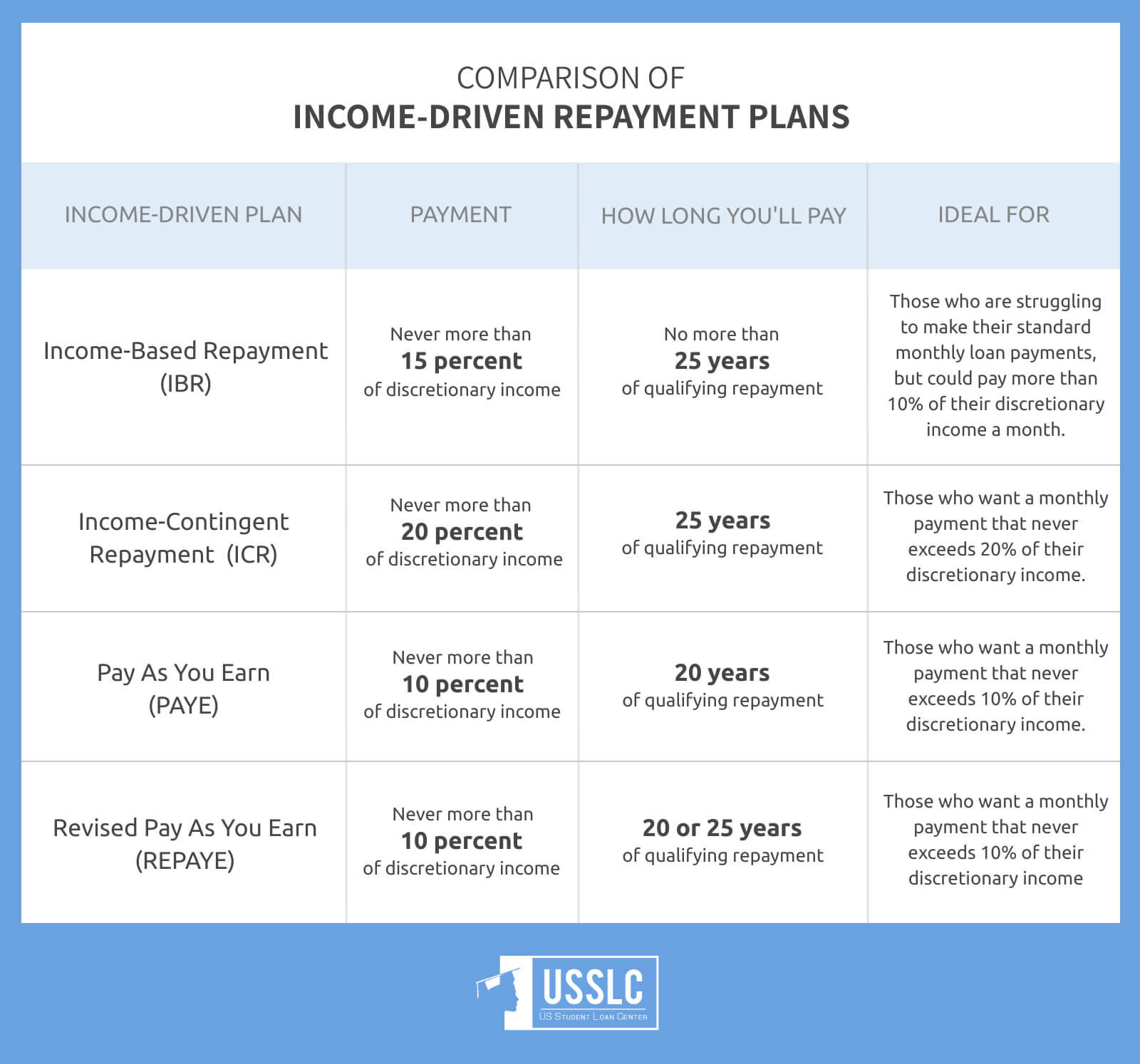

2. Enroll in an Income-Driven Repayment Plan: Income-driven repayment plans can be a great option for borrowers struggling to manage their student loan payments, including the accrued interest. These plans calculate your monthly payments based on your income, making them more affordable for many borrowers. By enrolling in an income-driven repayment plan, you may be able to lower your monthly payments and allocate more funds towards paying off the accrued interest.

3. Explore Loan Consolidation or Refinancing: Another strategy for managing unpaid accrued interest on student loans is to explore loan consolidation or refinancing options. Loan consolidation involves combining multiple loans into one, which can simplify your repayment process and potentially lower your interest rate. Refinancing, on the other hand, involves taking out a new loan with a private lender to pay off your existing loans. This can also help lower your interest rate and potentially save you money on interest payments over time.

It’s important to carefully consider the terms and conditions of loan consolidation or refinancing before making a decision. These options may not be suitable for everyone and could result in losing certain borrower benefits or protections offered by federal student loans.

4. Prioritize High-Interest Loans: When managing unpaid accrued interest on student loans, it’s important to prioritize high-interest loans first. By focusing on paying off the loans with the highest interest rates, you can minimize the overall cost of your debt over time. This strategic approach can help you save money on interest payments and pay off your loans more efficiently.

5. Seek Financial Counseling: If you’re struggling to manage unpaid accrued interest on your student loans, consider seeking financial counseling. A financial advisor or counselor can provide personalized advice and guidance on how to effectively manage your student loan debt. They can help you create a repayment plan, explore repayment options, and develop a budget that works for your financial situation.

Ultimately, managing unpaid accrued interest on student loans requires proactive planning and communication with your loan servicer. By exploring different strategies and staying informed about your options, you can effectively manage your student loan debt and work towards financial freedom.

Consequences of Ignoring Unpaid Accrued Interest on Student Loans

Unpaid accrued interest on student loans can have serious consequences for borrowers who choose to ignore it. These consequences can impact the borrower’s financial health and overall well-being. Here are some of the potential outcomes of neglecting to address unpaid accrued interest on student loans:

1. Increased Total Loan Balance: When borrowers fail to make payments on their student loans, the unpaid accrued interest is added to the principal balance of the loan. This means that the total amount owed increases over time, leading to higher monthly payments and a longer repayment period. Ignoring unpaid interest can result in a significantly larger loan balance than originally borrowed.

2. Negative Impact on Credit Score: Failure to address unpaid accrued interest can also have a negative impact on the borrower’s credit score. Late payments or defaulting on student loans can lower credit scores, making it harder to qualify for future loans or credit cards. A lower credit score can also result in higher interest rates on any new loans, costing the borrower more money in the long run.

3. Collection Efforts and Legal Action: If unpaid accrued interest continues to go unaddressed, the loan servicer may escalate collection efforts. This can include phone calls, letters, and potentially even legal action such as wage garnishment or the seizure of tax refunds. Ignoring unpaid interest can lead to a stressful and costly legal battle that can further damage the borrower’s financial situation.

4. Limited Financial Opportunities: Perhaps the most significant consequence of ignoring unpaid accrued interest on student loans is the limitation it can place on the borrower’s financial opportunities. A damaged credit score and a history of unpaid debt can make it challenging to secure loans for a home, car, or other major purchases. It can also impact the borrower’s ability to rent an apartment, obtain insurance, or even qualify for certain job opportunities that require a clean financial record.

Additionally, the stress and anxiety of dealing with unpaid student loan debt can take a toll on a borrower’s mental and emotional well-being. Constantly worrying about mounting debt and the repercussions of ignoring unpaid interest can lead to increased stress, depression, and overall decreased quality of life.

Overall, ignoring unpaid accrued interest on student loans can have far-reaching consequences that extend beyond just financial problems. It is crucial for borrowers to address any outstanding debt promptly and seek assistance from loan servicers or financial advisors if needed. By taking proactive steps to address unpaid interest, borrowers can avoid the negative consequences and work towards a more secure financial future.

Seeking Assistance for Unpaid Accrued Interest on Student Loans

Dealing with unpaid accrued interest on student loans can be overwhelming, but there are resources and options available to help borrowers navigate this challenging situation. Here are some tips on seeking assistance for unpaid accrued interest on student loans:

1. Contact Your Loan Servicer:

The first step in addressing unpaid accrued interest on student loans is to reach out to your loan servicer. They can provide you with information on your current balance, accrued interest, repayment options, and any available assistance programs. It’s essential to communicate with them to discuss your financial situation and explore potential solutions.

2. Explore Income-Driven Repayment Plans:

If you’re struggling to make payments on your student loans due to unpaid accrued interest, you may qualify for an income-driven repayment plan. These plans adjust your monthly payments based on your income and family size, making them more manageable. Contact your loan servicer to see if you qualify for this option.

3. Consider Loan Forgiveness Programs:

There are various loan forgiveness programs available for borrowers with federal student loans. Public Service Loan Forgiveness (PSLF) and Teacher Loan Forgiveness are examples of programs that forgive a portion of your loan balance after meeting specific requirements. Explore these options to see if you qualify for forgiveness of your unpaid accrued interest.

4. Seek Financial Counseling:

If you’re feeling overwhelmed by your student loan debt and unpaid accrued interest, consider seeking financial counseling. A financial counselor can help you create a budget, prioritize your expenses, and develop a repayment plan that works for your financial situation. They can also provide guidance on managing your debts and improving your overall financial well-being.

5. Look into Student Loan Assistance Programs:

In addition to income-driven repayment plans and loan forgiveness programs, there are other student loan assistance programs available to help borrowers struggling with unpaid accrued interest. These programs may offer loan consolidation, interest rate reduction, or temporary payment relief. Research and inquire about these programs to see if they can provide the assistance you need.

By being proactive and exploring all available options, borrowers can find the help they need to address unpaid accrued interest on their student loans. Don’t hesitate to reach out to your loan servicer, explore repayment plans, consider loan forgiveness programs, seek financial counseling, and research student loan assistance programs to find the best solution for your financial situation.